[ad_1]

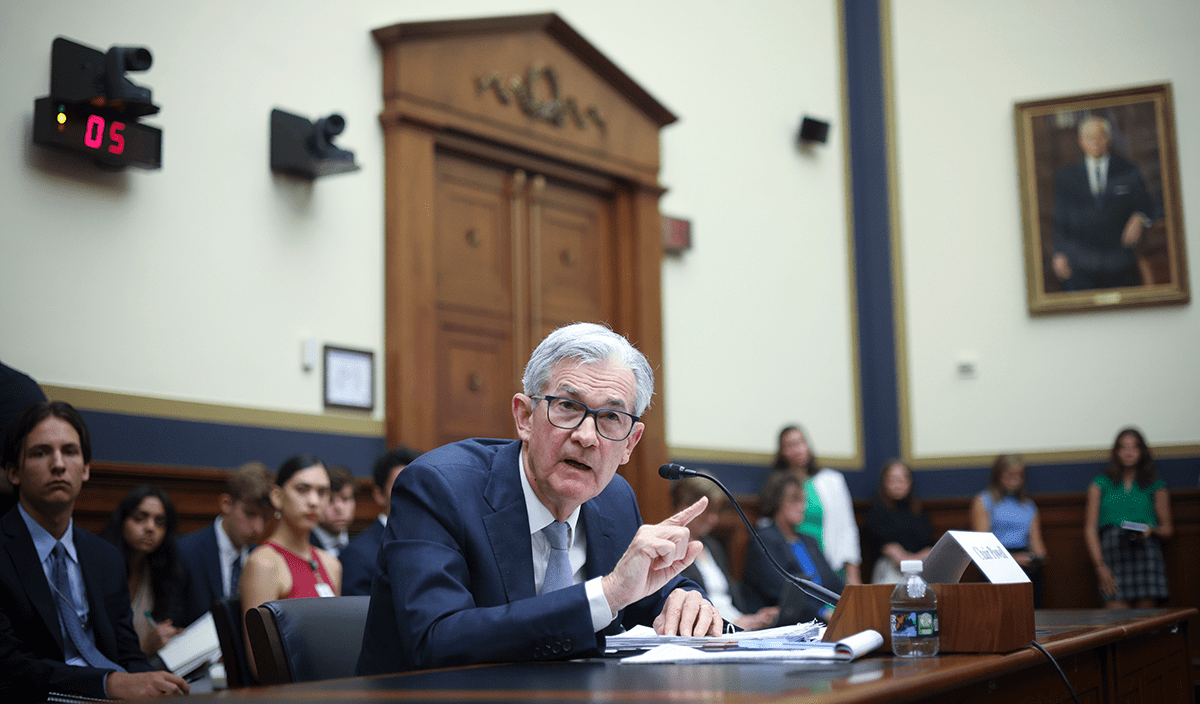

“Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century. These lessons are guiding us as we use our tools to bring inflation down. . . . We will keep at it until we are confident the job is done.” — Jerome Powell, 26 August 2022

In “The Eye of the Storm: The Fed, Inflation, and the Ides of October,” I recommended that investors temper their enthusiasm in response to a strong equity market rally and not underestimate the US Federal Reserve’s resolve in its battle against inflation. On 26 August 2022, Fed chair Jerome Powell spoke at the annual Jackson Hole Economic Symposium. His forceful language and deliberate references to the lessons of history laid to rest any hope that the Fed will shift away from its tightening strategy. Equity markets responded with sharp declines.

The Fed leadership has struggled over the last nine months to convince the markets that its dovish bias of the past 40 years no longer applies. What explains the communication challenge? Many investors simply do not understand that this is a rare and dangerous inflationary event. The inflation of 1919 to 1920 that followed World War I and the Great Influenza is the most relevant parallel. Although such major crises often lead to temporarily high inflation, the Fed still must act aggressively to contain it. Failure to do so could allow temporary inflation to transform into a repeat of the Great Inflation of the 1970s and early 1980s.

In his speech, Powell emphasized three distinct lessons from financial history that explain the Fed’s approach. By framing the speech around these lessons, he showed that the Fed recognizes the severe danger if inflation persists at today’s elevated levels, that it accepts its unique responsibility to eliminate this risk, and that it is committed to avoiding its predecessors’ mistakes regardless of the short-term pain that will likely entail.

1. “The first lesson is that central banks can and should take responsibility for delivering low and stable inflation.”

In the Fed’s 108-year history, the Great Inflation stands out among its gravest errors — rivaled only by the Great Depression. The flawed monetary policies of this period resulted, in part, from the common belief that the Fed was obligated to synchronize monetary and fiscal policy. When successive US presidents pursued overly expansionary fiscal policies, such as the Great Society and the Vietnam conflict, the Fed’s leadership hesitated to counterbalance them with contractionary monetary policy. In 1965, after the Fed pushed for higher interest rates (or cuts in spending), President Lyndon Johnson reportedly pinned the Fed chair, William McChesney Martin, Jr., against a wall at his Texas ranch and shouted, “Martin, my boys are dying in Vietnam and you won’t print the money I need.” When President Richard Nixon was asked whether he respected Fed chair Arthur F. Burns’s independence, he responded, “I respect his independence. However, I hope that independently he will conclude that my views are the ones he should follow.” Such coercion was not easy for the Fed to resist.

But Powell has now made it clear that central banks can and should take responsibility for delivering low and stable inflation, thus signaling that the Fed will resist any potential political pressure.

2. “The second lesson is that the public’s expectations about future inflation can play an important role in setting the path of inflation over time.”

Powell understands the enormous risk long-term high inflation poses to the US economy. The Fed’s experience during the Great Inflation is instructive. Under Martin, the Fed had the opportunity to extinguish inflation in the late 1960s. It failed to act, and its inaction did not go unnoticed: Market participants began incorporating higher inflation expectations into their future plans. Once higher inflation was entrenched in the economy, it became much more difficult to unwind. Indeed, Fed chair Paul Volcker had to raise interest rates all the way to 20% in 1981. History shows that lowering inflation expectations requires much more aggressive and sustained monetary tightening. That’s why it is critical to prevent higher inflation expectations from taking root in the first place. Powell’s statement shows the Fed is aware of this risk and recognizes that time is running out.

3. “That brings me to the third lesson, which is that we must keep at it until the job is done.”

“Keep at it” evokes Paul Volcker, the Fed chair who triumphed over the longest lasting inflation crisis in the nation’s history. This reference reveals that Powell understands the severe consequences of the Fed’s half-hearted efforts to tighten monetary policy under Martin and Burns. The truth is that the Fed’s leadership in the 1960s and 1970s understood that inflation was damaging; they were just unable (or unwilling) to bear the costs of ending it. Each time they engaged in monetary tightening, they prematurely reversed course in response to rising unemployment. The public correctly interpreted the Fed’s lack of resolve as a sign that high inflation would continue. By the time Volcker announced a new strategy in October 1979, it required several years of pain to convince the public that he was serious.

Powell’s recognition that the Fed “must keep at it until the job is done,” sends a clear message that a potential recession or uptick in unemployment will not stop the Fed from further monetary tightening. The Fed’s primary goal is to reduce inflation to its 2% target. An economic recession and job losses are, in Powell’s words, “unfortunate costs of reducing inflation.” These costs are worth it, however, because “a failure to restore price stability would mean far greater pain.” Those who recall the stagflation years of the 1970s can attest to the fact that one day we will be thankful for the Fed’s resolve.

Future Outlook

Powell’s statement at Jackson Hole reiterated that the Fed leadership understands why the Great Inflation happened and how painful it will be if it happens again. It also asserted the Fed’s independence, that it is obliged to do whatever it takes to prevent the United States from a repeat of 1970s-style inflation.

Those who doubt the Fed’s determination may wish to reconsider their thesis. The Fed showed its hand in Jackson Hole, and it is a strong one. Investors would be wise to brace themselves for more aggressive monetary tightening until inflation is extinguished. This will likely mean more economic pain. Of course, the key lesson of the Great Inflation of 40-odd years ago is that the pain is worth the long-term gain.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author. As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Image credit: ©Getty Images/Win McNamee/Staff

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Source link

Bitcoin

Bitcoin  Tether

Tether  USDC

USDC  Dogecoin

Dogecoin  LEO Token

LEO Token {kind=link}

{kind=link}

{kind=link}