[ad_1]

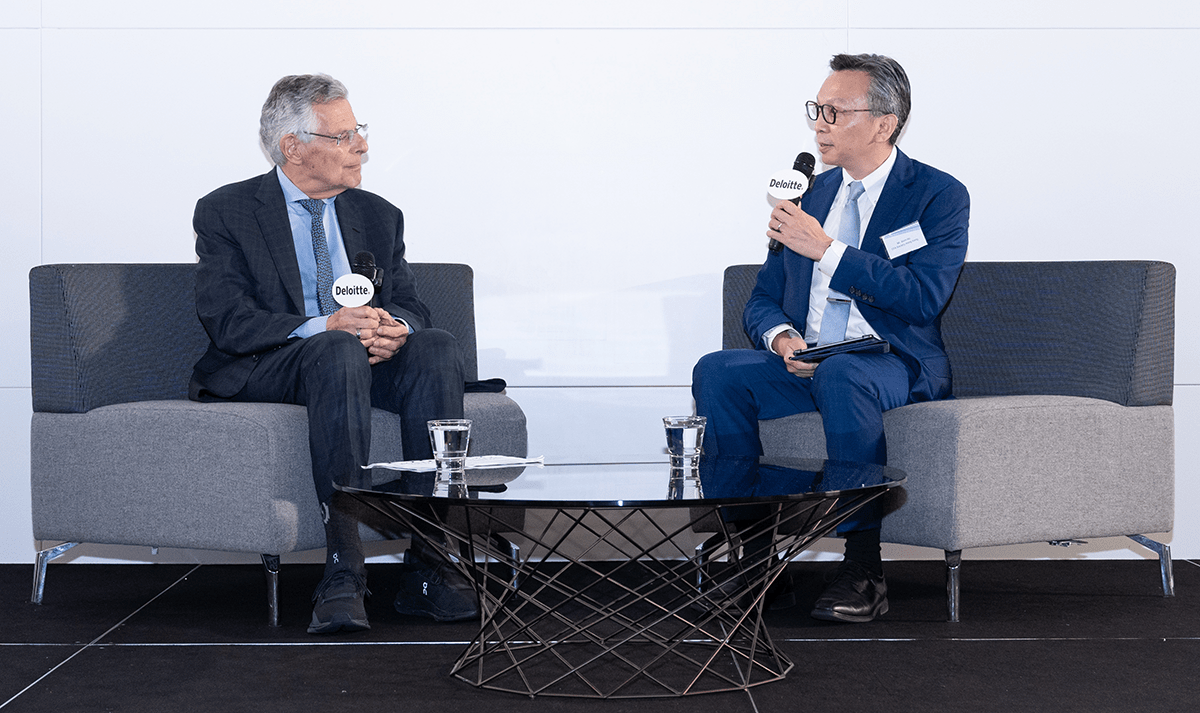

Through his examinations of how uncertainty influences asset prices, Nobel laureate Myron Scholes has helped revolutionize our understanding of the financial markets. His development of the Black–Scholes options pricing model with Fischer Black more than half a century ago redefined how investment professionals do their jobs and opened up a new era in the world of finance.

Even though he is one of the most influential living economists, Scholes is not resting on his laurels. His explorations of the inner workings of the financial markets continue, with a particular focus on both artificial intelligence (AI) and carbon credits and how they compare with options, among other phenomena.

He recently participated in a wide-ranging fireside chat arranged by Janus Henderson,hosted by CFA Society Hong Kong, and moderated by Alvin Ho, PhD, CFA. The conversation, which took place on 3 July 2023 in Hong Kong, covered both the continued relevance of the Black–Scholes model 50 years after its unveiling as well as Scholes’s current research interests. Below is a lightly edited transcript of the discussion.

The Black–Scholes Revolution

CFA Society Hong Kong: It has been 50 years since you published the famous Black–Scholes model, and it remains one of the most popular readings among financial professionals. How did that happen?

Myron Scholes: The model was really about explaining how to price options, but I’m happy that it has changed the banking landscape from an agency-only to a principal business.

Now, if you think about it, uncertainty is the most important thing in your life. The mean is nothing! Having options to deal with uncertainties and risks is so important. If life were unchanging, then options would not be as valuable, but life is always changing, which makes options and the ability to deal with uncertainties very precious.

With the Black–Scholes technology, we can help clients figure out what exactly they want and how to offset the delta and risks associated with it. Essentially, I see the options market as a crowd-sourcing place to determine what level of risk the market is signaling and subsequently help business owners to make decisions.

Decarbonization and Portfolio Construction

Going into your decarbonization and portfolio theory, how does the work that you have done in the options space help here?

I have done a lot of risk–return portfolio theory. To me, understanding constraints is of the utmost importance. You do not need to be a better forecaster than everyone else, but you do need to understand the constraints of others. For example, if people are constrained, if they trust you, they would be willing to pay you to take their constraints off. That’s when your options are valuable. This ability to unconstrain the constrained also happens in parenting and M&A.

If you want to make money in your life, being “boring” is important. You wouldn’t want the choppiness of your life affecting your returns, but you would want to smooth the volatility of returns and cut the tails. If you managed to do that, your compounded return would be so much better. My options theory is really meant to help understand the tail. If you think about decarbonization, we also want to smooth the path to decarbonization, and one way to do that is to create more paths to achieve it, and to some extent, it’s quite like a put option.

Myron, to dive deeper into the same topic, I want to ask a three-part question. First, how should investors determine the fair value of carbon credits?

Market efficiency is my core belief, and I do think it’s a good way to determine fair value for carbon credits. However, the problem is when we have cheaters coming into the market. We need teams and infrastructure to sort out the good and bad credits. Like the fixed-income market, we will have the whole hierarchy in the system. We have a credit rating agency to rate corporate fundamentals and allow investors to choose what level of risk and credit they would like to be involved in. After all, I’m not saying market price should always equal the fair value, but the market price usually gives you a good anchor point to determine that.

Speaking of the origin of the option formula that helps price options: People kept saying to me, “You should keep it to yourself.” I said to myself that I could have made more money doing other things. Hence, I decided to share it with everyone.

Some guys said they had a solution before you did.

Yes, they said that, but they could never prove that. You see: Every successful idea has a thousand fathers, and every bad idea is mine.

Are you in the camp that every carbon credit is different, or does the quality of the forest also matter?

Decarbonization is about taking carbon out of the system. We shouldn’t care about where the carbon came from or where it is being taken away from. Eventually, all we need to know is what is the net carbon and how much it can contribute to decarbonization. The way I think about a carbon credit is that it is a commodity to me. I don’t care where it comes from; just get it graded, and that’s my credit. We should commoditize it just like any other commodity in the market. It should just be a matter of time before carbon credits become a commodity.

As portfolio managers, how should we determine the optimal allocation or risk budget for carbon credits? Do you think that should be a decision made by the asset owners themselves?

From what I devised in my paper and through a reference, it is a mechanism for individual choice. It puts in place the separation of the carbon problem from the portfolio problem. You can tell your client so that individuals can make their own decisions based on the two different portfolios — a regular portfolio and another one with carbon net zero. Not everyone should be doing the valuations of carbon credits. You, as a portfolio manager, can hire people to do that. You can separate the problems of portfolio management and decarbonization to make your judgment. By separating the two problems, you also benefit from efficiency and economy of scale.

Relative to buying credits, many corporations, such as Microsoft and Google, instead of trading the carbon credit, they retire it so that the carbon quota is “physically removed” to conserve the environment. Do you think by trading it, portfolio managers defeats the purpose of environmental conservation?

In theory, what we want to do is to create a system for society to reduce carbon emissions. Many smaller firms, though, have no capabilities to do that. What I envision in the future is that advisers will come in and help the small companies do it with the portfolio and a blockchain system to use the credit. Everyone can have a more sustainable business when they use the credits and contribute to decarbonization.

Three Fallacies of Data Mining and AI

Recently, we have seen many discussions of the rise of private markets. Level III of the CFA Program exam will have private markets as one of the three specialized pathways. In private markets, particularly private equity and venture capital, there is much discussion on using modern technology to improve data analysis or to refine valuations. Last time you spoke at CFA Society China, you talked about the data mining problem. Do you think big data science will help solve the problem or make it worse?

There are three fallacies in our industry, and one of them is data mining. We always look at the legs of the elephant and think the whole world is the legs of the elephant. I now know there is a similar Chinese saying. In truth, compared with people in the future, what we know is very limited. Future generations must learn from a new perspective. We don’t want them to learn what we learned and become one of us. Let them see a different part of the legs.

Regenerative AI will help us analyze the past much more efficiently. With that technology, future generations can utilize their time much more efficiently and not have to do regression by inverting matrices by hand, a stupid thing I did.

The second fallacy is the clustering fallacy. We put data in boxes we created. They do not come from nature. We are cheating. It is called an NP-complete problem in computer science. As the number of boxes goes up exponentially — and they may have taught you at Tsinghua University, Alvin — the boxes and the data can be corrupted and give you incomplete and wrong solutions.

The third problem is that every model we develop has an error term. But after a while, people reverse-engineer the model to figure out how to game it against us. They destroy the validity of the model’s error term by making money at the expense of those with the error term in the model.

So, with these three problems, you have got to be careful using ChatGPT because people can cheat and beat the error of the model.

The interesting thing is that everything in life is volatility times time. As volatility increases, time compresses. But what we care about is the validity of the fixed point. If we lose it, everything in the past becomes meaningless. As things change, we have to reestablish a new fixed point, and AI hasn’t figured that out. It is wired such that, at least up to now, we humans have been able to restart time and figure out what the new fixed point is. AI can’t, yet. That’s where creativity comes in.

Finally . . . Parenting

As you have pre-empted my questions about AI, I only have one more question for you. For the parents and the young executives in the audience, would you advise their kids and the executives, respectively, to change lanes and study data science rather than, say, economics?

It all depends on personality. Some people would enjoy being a farmer or even a hunter. I, myself, am a hunter, in a logical sense, by taking risks. There was a time that I was in Washington, DC, and the officials explained the rules and what could and could not be said, and I thought it wasn’t for me, so I left.

I’m a hunter who loves exploring and looking at possibilities. You have to know what you like and take it from there.

Thank you, Myron.

The CFA Society Hong Kong thanks Janus Henderson for arranging the event. Volunteers, including Lin Ning, CFA, Felicia Wong, CFA, Adam Wong, CFA, Jeffrey Tse, CFA, and Gilbert Wong, CFA, provided inputs to the preparation.

If you liked this post, don’t forget to subscribe to the Enterprising Investor.

All posts are the opinion of the author(s). As such, they should not be construed as investment advice, nor do the opinions expressed necessarily reflect the views of CFA Institute or the author’s employer.

Images courtesy of CFA Society Hong Kong

Professional Learning for CFA Institute Members

CFA Institute members are empowered to self-determine and self-report professional learning (PL) credits earned, including content on Enterprising Investor. Members can record credits easily using their online PL tracker.

[ad_2]

Source link

Bitcoin

Bitcoin  Tether

Tether  USDC

USDC  Dogecoin

Dogecoin  LEO Token

LEO Token {kind=link}

{kind=link}

{kind=link}

{kind=link}